A Hidden Tax Increasing

California Businesses Face 247% Increase in Federal Unemployment Insurance (UI) Tax

California employers are about to pay a lot more in unemployment insurance taxes because the governor and Legislature have failed to pay down a massive $21 billion debt in the Unemployment Insurance (UI) Fund. The UI Fund is the most important safety net that workers have, and it is paid for entirely by employers. A variety of policy decisions by the Legislature and previous administrations already placed the UI Fund on shaky fiscal footing by expanding benefits without paying for them, but the unprecedented burden placed on the Fund during COVID, and political decisions made after the fact, likely will keep the Fund insolvent for decades.

While COVID was unprecedented, the state’s response to the UI Fund debt is a crisis of our own making. As discussed below, the federal government responsibly provided COVID funds to help states pay down their debt, which reduced the burden on businesses recovering from the pandemic and strengthened this vital safety net program for millions of residents. Governor Newsom and the State Legislature made different policy choices. And now, all employers—small and large—are paying the price in higher premiums which is a new hidden tax from the Legislature and governor.

How the Tax Works

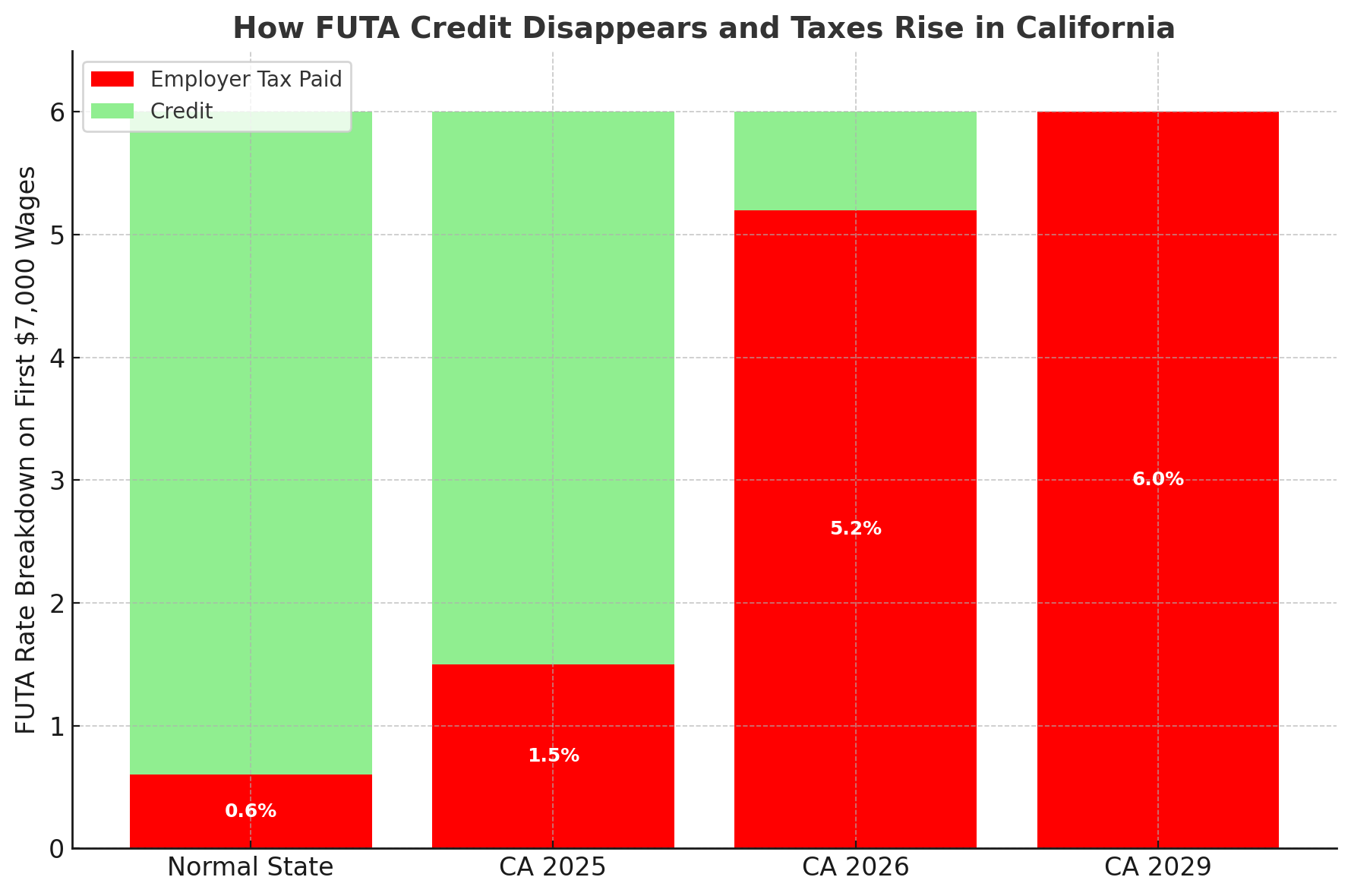

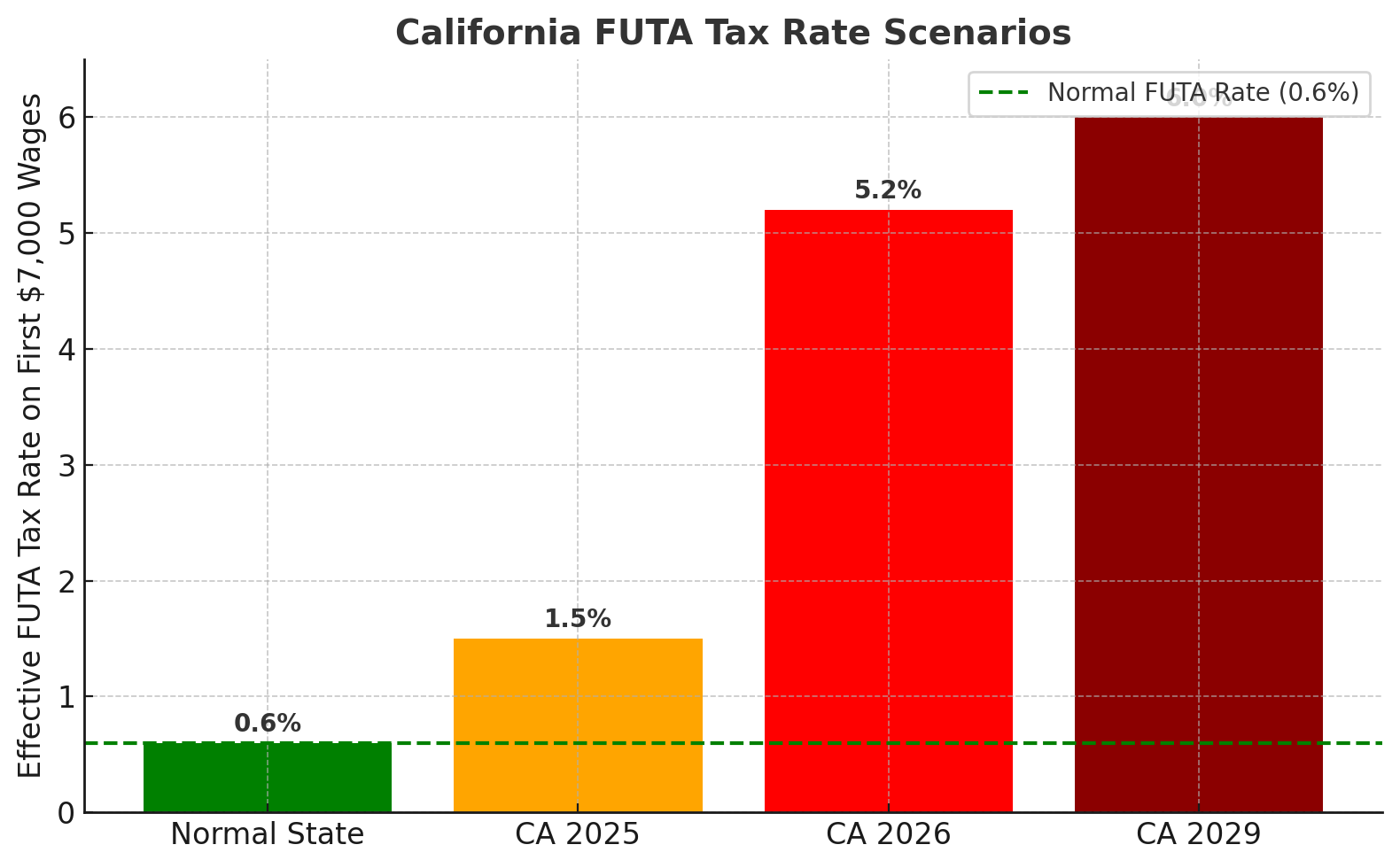

Normally, employers pay a federal unemployment tax (FUTA) of 6.0% on the first $7,000 of each worker’s wages. However, employers normally get a 5.4% credit if their state’s unemployment insurance fund is healthy. That credit reduces the FUTA rate to 0.6% (≈ $42 per worker per year).

Because California politicians chose not to pay off the debt with the billions in surplus dollars we had at the time, we still owe billions in federal loans. In short, our Fund is far from “healthy.” As a result, employers are losing their FUTA credit. The tax rate is already up to 1.5%—more than double the normal rate.

If the debt isn’t paid, the rate will continue climbing every year by 0.3 percentage points. That means it will rise to 1.8% this year.

The Bigger Penalties Coming

But it doesn’t stop there. States like California that keep carrying debt face additional penalties:

After 3 years, the federal government can add a 2.7% increase. The Biden Administration waived this penalty once, but it could come back.

After 5 years, another formula called the Benefit Cost Reduction (BCR) kicks in. For California, the BCR is estimated at 3.4%, far higher than New York (1.1%) or Connecticut (0.8%).

Bottom line: California employers could soon pay a FUTA tax of 5.2%, compared to 0.6% in nearly every other state. That’s a 247% increase from today’s rate.

Why This Happened

During the pandemic, the federal government gave states money to pay down these debts. Almost every state used those funds responsibly. Texas, for example, not only paid off its debt but rebuilt its UI fund for the future.

Governor Newsom and the Legislative leadership chose to use the money for their budget priorities knowing that employers would pay their price in the end. That is the new hidden tax. Now, instead of shrinking, the debt is projected to hit $21 billion by the end of 2025.

A recent State Auditor’s report found the Employment Development Department (EDD) made serious accounting mistakes, misstated billions in liabilities, and lacked basic financial controls.

Who Pays the Price

Employers must pay higher federal taxes, especially those with high turnover, like seasonal industries (tourism, agriculture, hospitality). Each time they hire someone new, the $7,000 taxable base resets.

These costs will ultimately flow to workers and consumers through lower wages, fewer jobs, and higher prices.

Why It Matters

California workers rely heavily on unemployment insurance. The state:

Has had the highest unemployment rate in the nation (above 1 million unemployed for 20 straight months).

Represents 20% of all unemployment claims nationwide, even though it has less than 12% of the U.S. workforce.

The state’s UI fund is effectively bankrupt. In 2025, it expects to pay out $6.8 billion in benefits but take in only $6.5 billion—deepening the hole.

The Takeaway

Because California leaders failed to manage its unemployment fund responsibly, employers here face some of the highest employment taxes in the country—and the bill is only getting bigger.

At the same time, there cannot be an increase in employee benefits (if needed) because it will only make the debt more unmanageable.

Most importantly, if California experiences major economic uncertainty or a recession the demand for benefits will skyrocket. In this situation, California would need a federal bailout from the Trump administration – or raise rates on employers again which would directly impact an economic recovery and future hiring.